Tether has been the subject of multiple investigations over the past few years. Most fit in at least one of these categories:

Currency issuance practices

Lack of corporate transparency

Reserves auditability difficulties

Loss of funds due to security breaches, enforcement actions, and questionable banking practices

Lack of KYC/AML mechanisms

Various civil and criminal charges against organizations linked to Tether and Bitfinex

Our main assumption when it comes to understanding the motives of the Tether creators is that no elaborate fraud schemes are needed when you can run a fractional reserve system and collect trading fees. We focus our attention on showing the role Tether plays in the crypto market without attempting to attribute individual crimes and securities laws violations to individual ecosystem participants.

Our findings

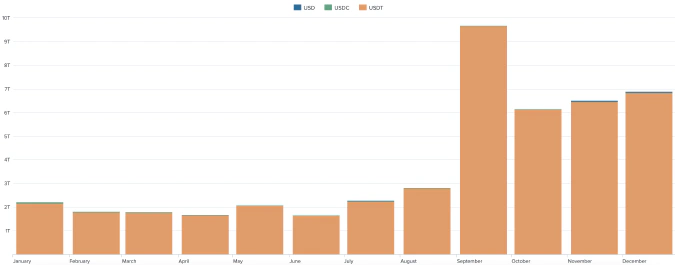

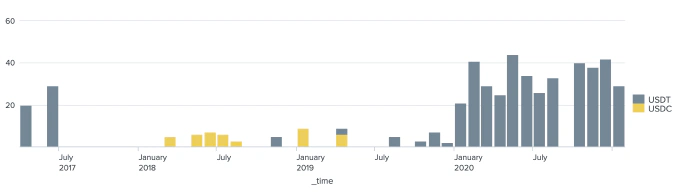

Dominance over USD markets

Tether is replacing fiat as a quote currency. It has the most liquid markets with $100B+/day trade volumes. It thrives anywhere traders struggle with banking access to fiat and is beginning to rival USD in developed markets.

Market Manipulation

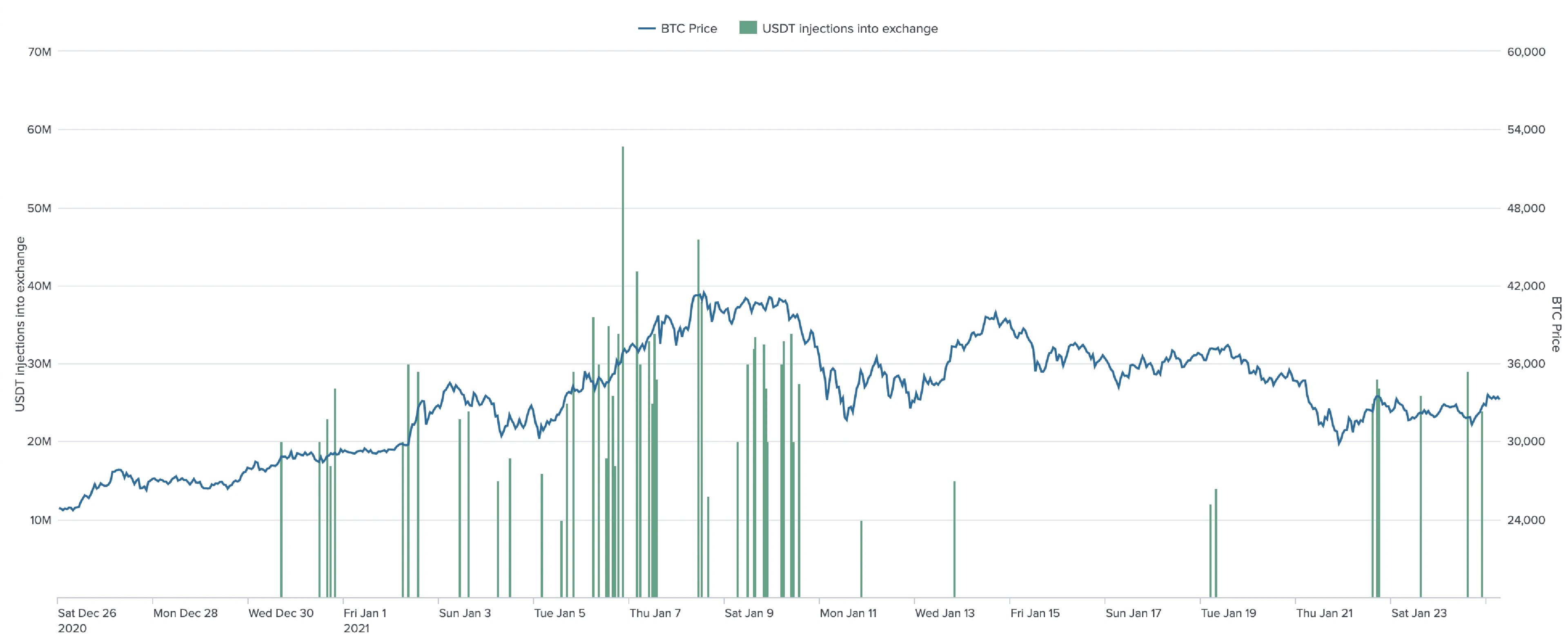

There is no statistical evidence that Tether minting is correlated with Bitcoin price moves beyond a typical supply-demand relationship. Moreover, correlation does not equal causation. Constantly evolving crypto-trading fundamentals make the correlation difficult to discern, and near-impossible to prove market participants’ motives.

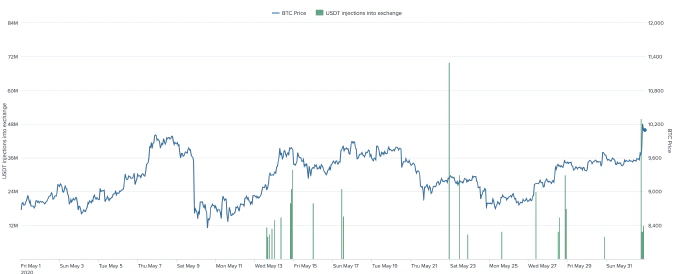

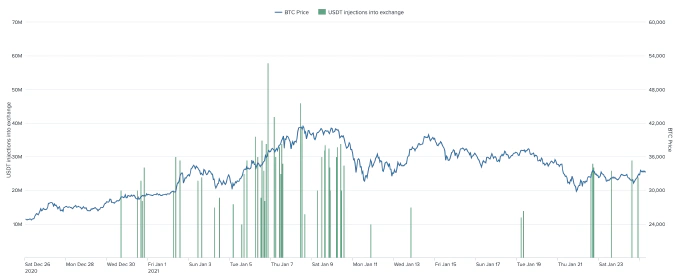

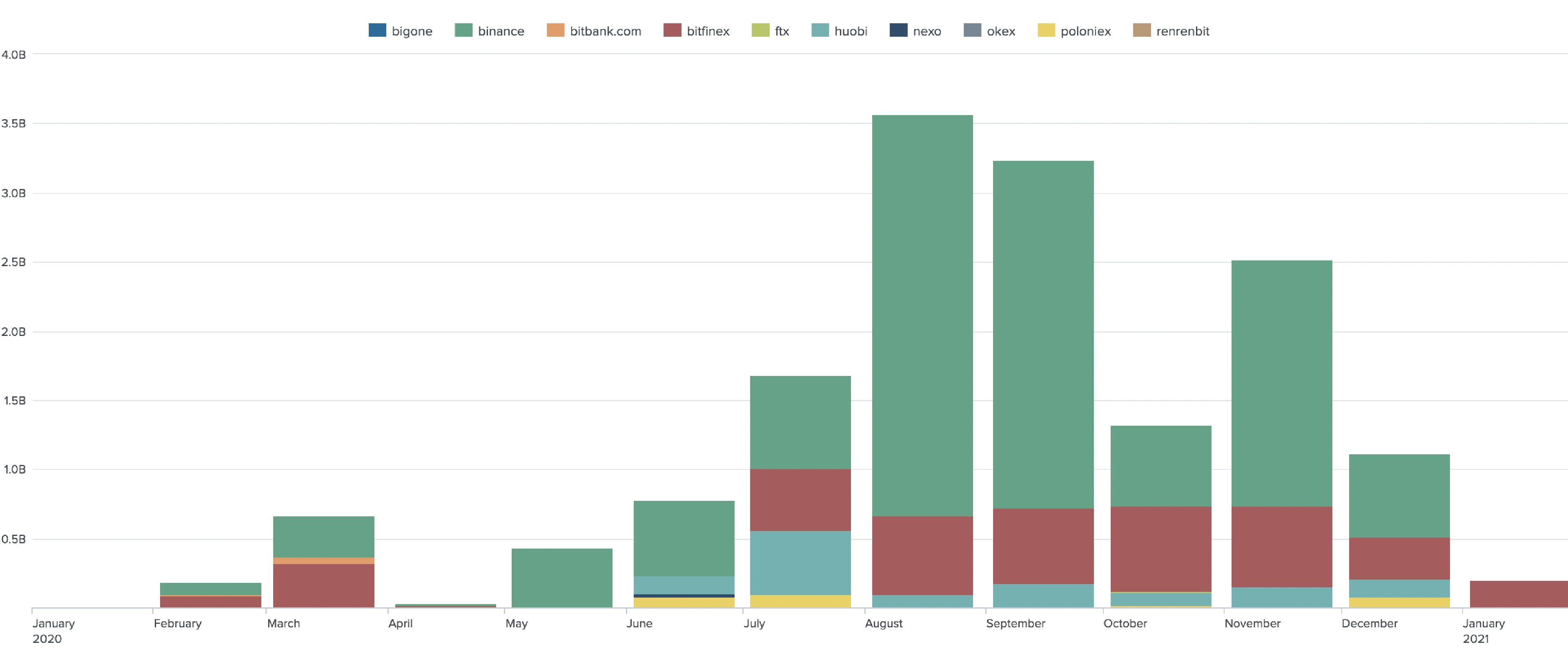

There is no suspicious pattern in the way Tether is liquidated beyond the lack of US- and EU-based trading venues. Major liquid exchanges in jurisdictions with liberal digital asset laws are involved in injecting Tether into the market. This also confirms the previous finding - Tether issuers are more concerned with quickly liquidating freshly minted Tether at a good price rather than financial market manipulations.

Legal Problems

Gambling

Tether is also actively used in the gambling industry. Multiple online gambling websites in China used Tether for its large cross-border transfers and laundering money. In the first nine months of 2020, the Chinese authorities cracked down on 1,700 online gambling platforms and 1,400 underground banks that processed over $153B for criminal organizations involved in illegal online gambling.

Drug trafficking

In Oct 2020, the DoJ unsealed a document alleging that a drug cartel that had been laundering money for 12 years attempted to bribe US officials and purchase US passports using Tether.

Capital Controls Evasion

Tether is pegged to the US Dollar, which offers a way to sidestep sanctions and capital controls (maximum $50,000 in yuan converted to a foreign currency per year in China) eliminating volatility risks. Up to $30M worth of USDT a day is traded on Moscow’s OTC trading desk by Chinese importers in Russia. Tether (which maintains parity with the US dollar) is bought in large batches to be sent back to China where there are strict capital controls. According to Head of OTC trading at Huobi Russia’s claim, Chinese clients come with cash, the prices at exchanges are registered, and the client’s money in USDT is sent to their wallet address in China. Back in China, the USDT can easily be converted into fiat again (Huobi and OKEx offer OTC trading desks). Such deals partly explain why there is huge USDT daily trading volumes, often exceeding its supply.

Loss of custody funds

One of the ‘third-party’ payment processors Tether used was a Panamanian entity called Crypto Capital Corp. Tether established a relationship back in 2014. By 2018, there had already been more than $1B of customer and corporate funds commingled with Crypto Capital.

As stated by Bitfinex and Tether, no written agreement was signed between Crypto Capital and Tether. By 2018, Bitfinex already had problems honoring customer requests to withdraw money from the platforms, as Crypto Capital was unable to process them. Despite these problems, the exchange claimed the withdrawals were processed as usual.

According to the documents provided by respondents, a senior Bitfinex executive was told by someone from Crypto Capital that $851M couldn’t be returned, as the funds were seized by government authorities in Portugal, Poland, and the United States.

Bitfinex never disclosed this loss of funds. Instead, Bitfinex and Tether (with the same executives in both firms) agreed upon a transaction from Tether to Bitfinex to cover up the losses (no repayment details were specified during the meeting) which raised questions about conflict of interest.

The NY Attorney General’s investigation into Tether is nearing completion. USDT-associated entities will most likely face hefty fines and will need to change their business practices in order to avoid further prosecution. The chance of the NY Attorney General finding nothing questionable in 2.5M documents that Tether had to hand over to them, we believe, is extremely low.

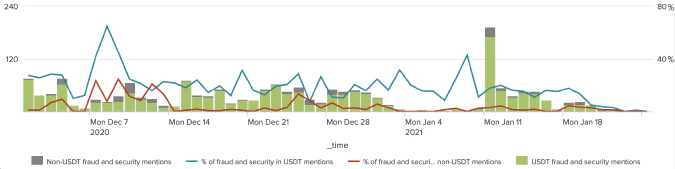

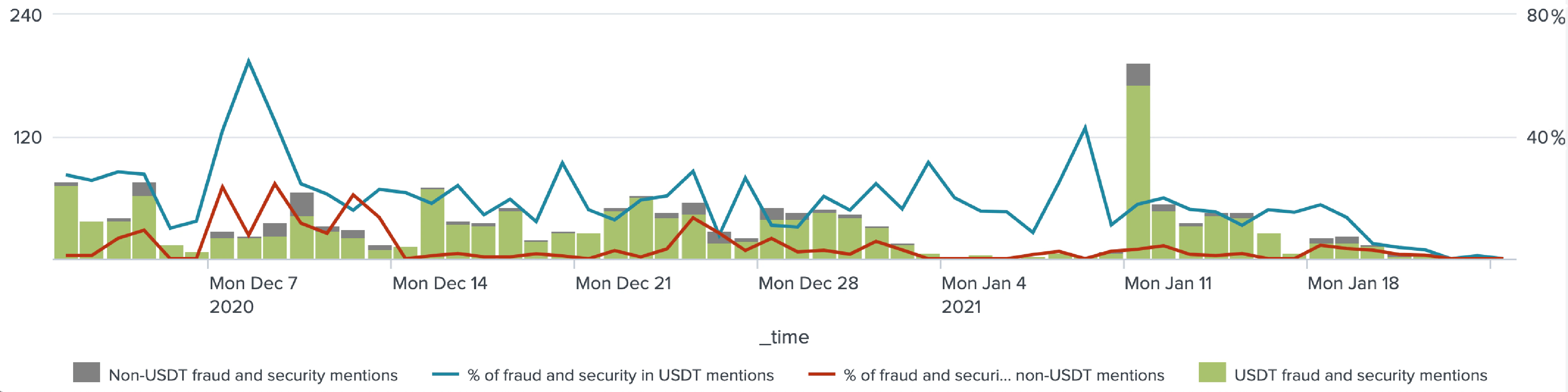

KYC/AML Obstacles

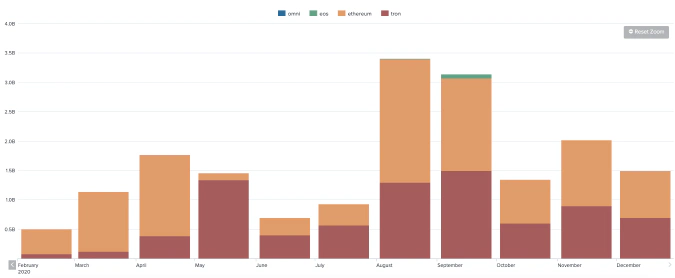

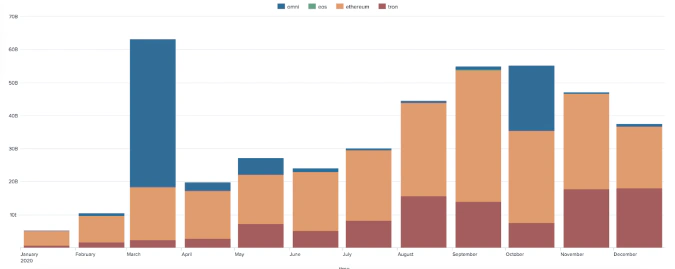

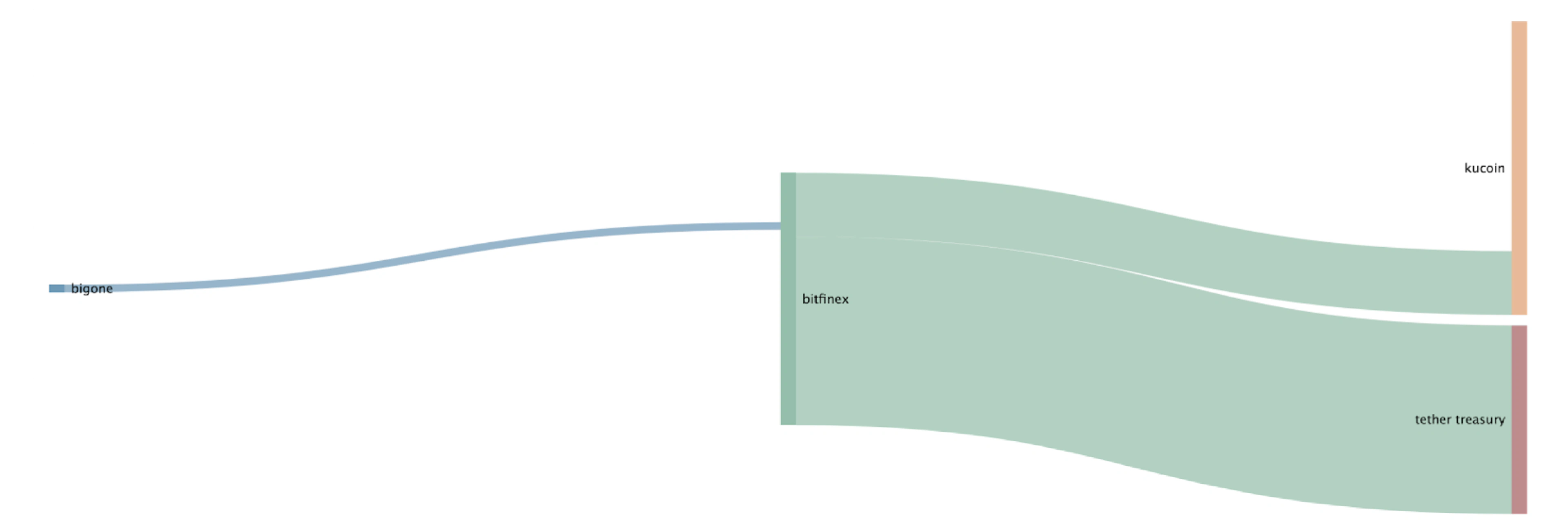

Deployed KYC/AML tools are struggling to keep up with millions of transactions per day. Most Tether use is seen in poorly-regulated markets with little to no surveillance. To further complicate the matter, in addition to Ethereum, Tether also uses other blockchains, including Omni, Tron, Algorand, Solana, EOS, OMG and Liquid networks.

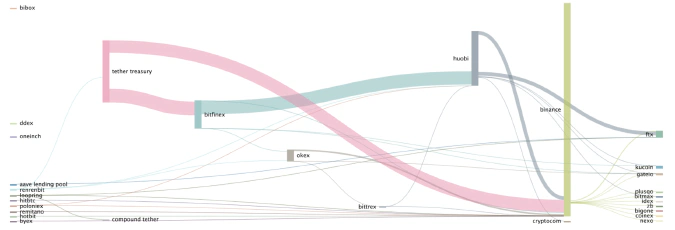

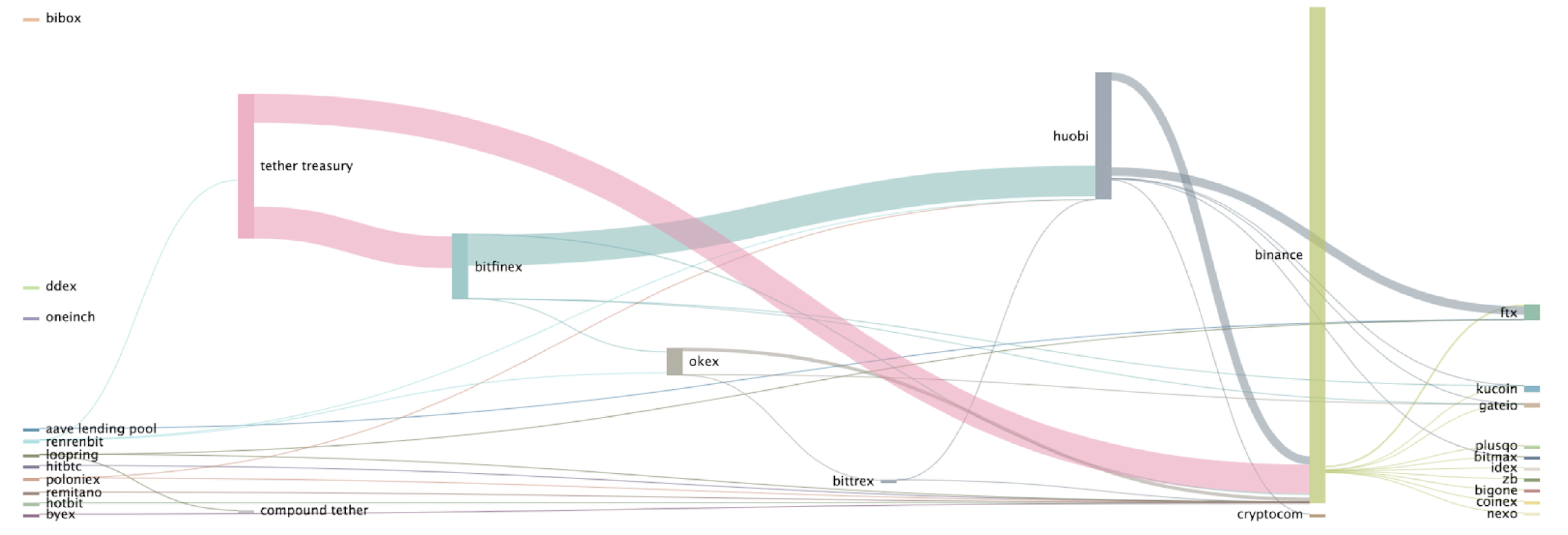

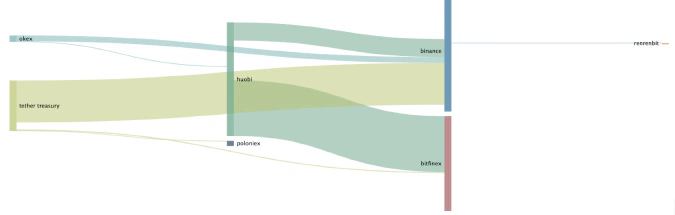

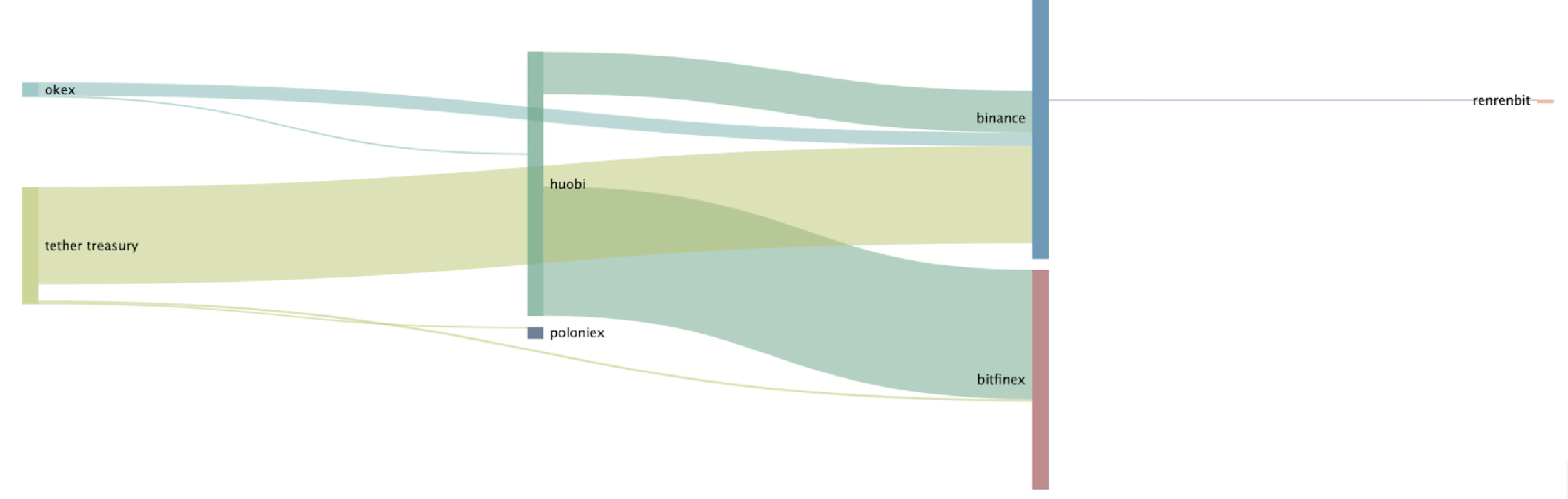

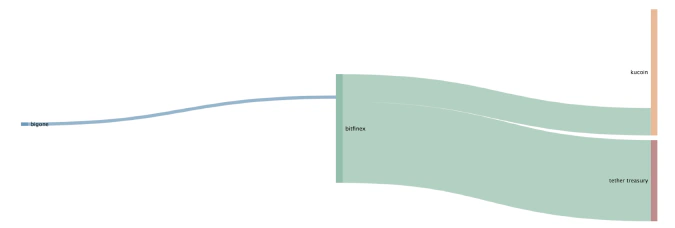

The diagram below demonstrates that USDT is already deeply integrated into the TRON network via transfers executed among major exchanges.

Conclusion

Tether is beginning to become a threat to fiat as a value transfer mechanism. Central Banks’ inability to introduce a viable alternative of USDT to the crypto market led to its overwhelming marking dominance. There is significant evidence that USDT is where money laundering is occurring. USDT’s use for massive cross border remittances is preferable to other coins like BTC because its price is stable. Tether does not require any centralized KYC for people using USDT, as there is no reliable method for identifying launderers from traders, without getting data from exchanges using USDT.

Allowing Tether to thrive for years led to new resilience mechanisms. Today, Tether is already in use on five independent blockchains, often dominating their on-chain transactions, and, in some cases, causing network congestion. Current blockchain forensics and market surveillance tools are unable to provide acceptable levels of KYC/AML efficiency. These tools fail to identify money laundering as an activity beyond attributing mixers to this sort of activity. This is a naive view of money laundering on crypto markets which significantly undervalues this activity as shown by Chainalysis’s 0.34% value for illegal activity.

Going after Tether issuers will require a significant international law enforcement and technical effort. However, such an attack will only push market participants to even more enforcement-resilient stablecoin alternatives. Any attempt to decrease crypto market reliance on USDT needs to be accompanied by offering stablecoins onshore in the US.