Introduction

The Inca Digital CBDC Factbook is a compilation of intelligence insights on international efforts to create Central Bank Digital Currencies. Most of the information presented in the Factbook is derived from natural language, financial, and technical datasets collected, cleaned, and enriched by Inca Digital. It relies heavily on the combined experience of Inca team members in software development, finance, and intelligence. Unlike other attempts to aggregate CBDC information, our Factbook is mostly focused on datasets, graphs, and diagrams, rather than political analysis.

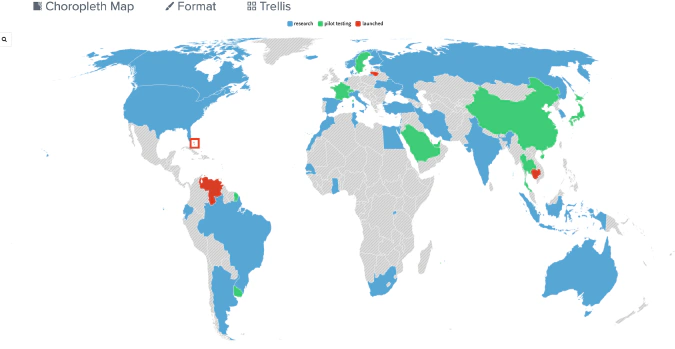

CBDC Tech Tree

In order to quantify the progress made by CBDC issuers, we have put together a diagram with technological, legislative, and usage milestones. These milestones include important components of any CBDC and serve as independent progress indicators.

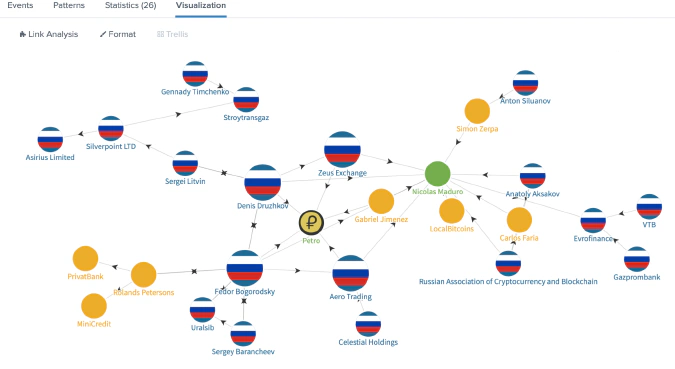

Although each CBDC development process is unique and might not perfectly fit in the diagram, the redundancy provided by 3 independent indicator categories ensures that progress on any given project will not go unnoticed. For example, although Russia has made little visible progress issuing a Digital Ruble, their hands-on technical experience obtained while assisting Venezuela with the Petro puts them next to other leaders in the CBDC race.

Ledger models

Some of the more radical differences between CBDCs span from their ledger design choice. Generally speaking, there is a whole spectrum of ledger architectures, from highly centralized to fully distributed. The most important part of the protocol design to watch, however, is the transaction validation component.

Centralized

Most of the upcoming CBDC projects opt for a centralized ledger built from scratch. While many of them might involve a 3rd party to perform various functions, they almost invariably retain full control over which transactions are considered valid. This will result in a central bank’s ability to credit any blockchain address, suspend it, or reverse previously valid transactions at any time.

Decentralized

Some issuers chose not to create their own ledger and, instead, rely on existing distributed ledgers and their validators. While this approach allows issuers to quickly integrate into the existing crypto ecosystem and gain adoption, it also significantly limits their ability to influence user behavior. Even in these situations, CBDC issuers retain control over the associated smart contracts, allowing them to freeze addresses and exercise other forms of capital controls.

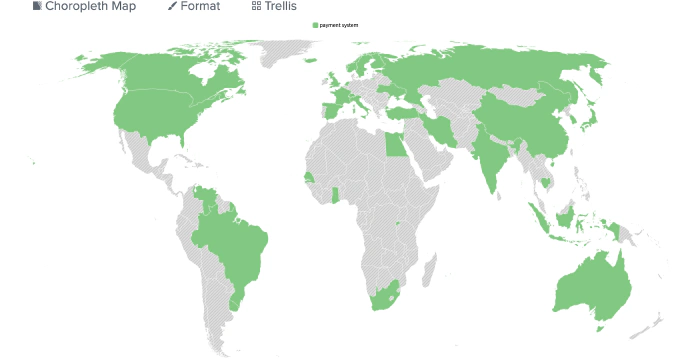

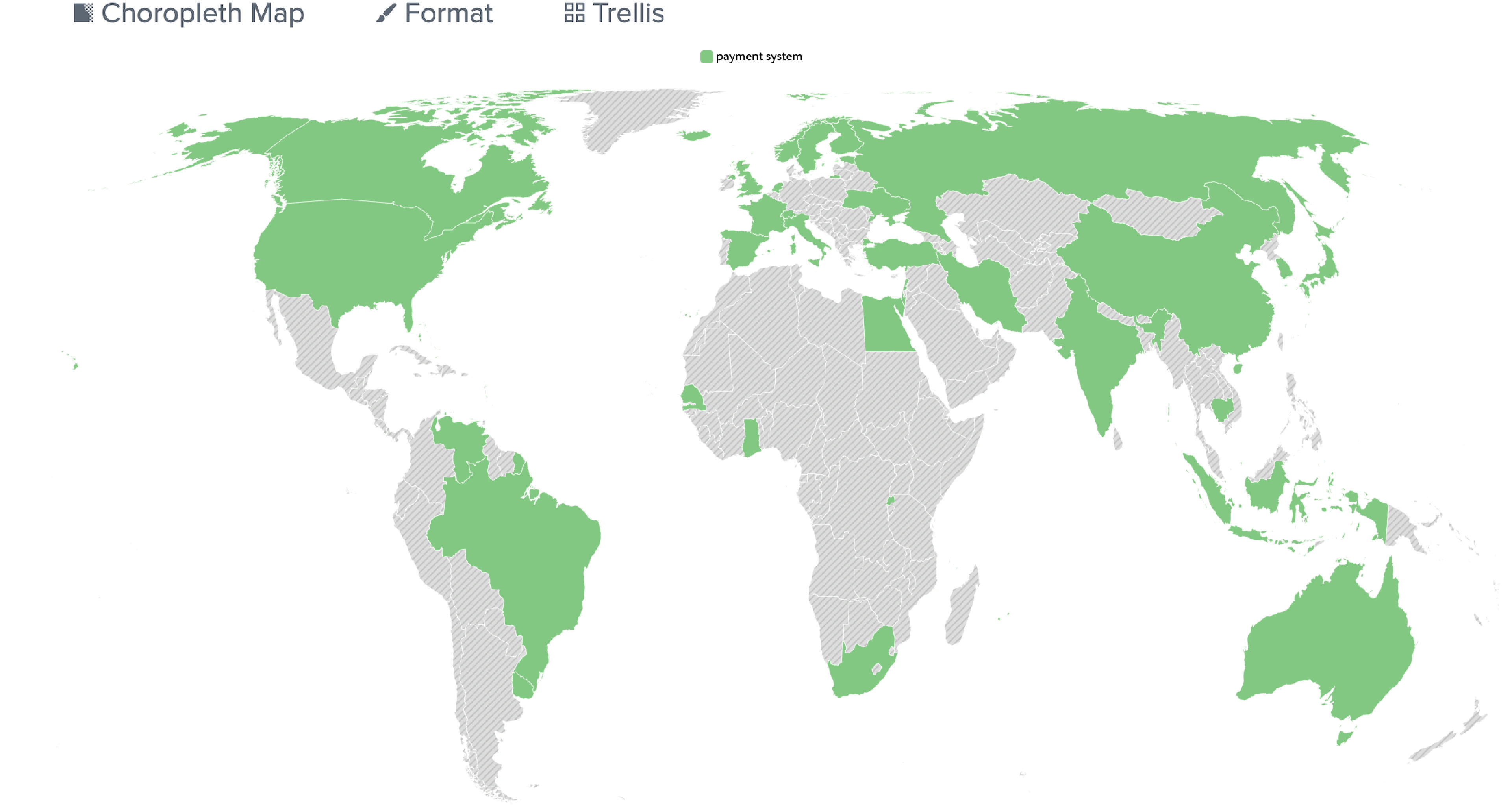

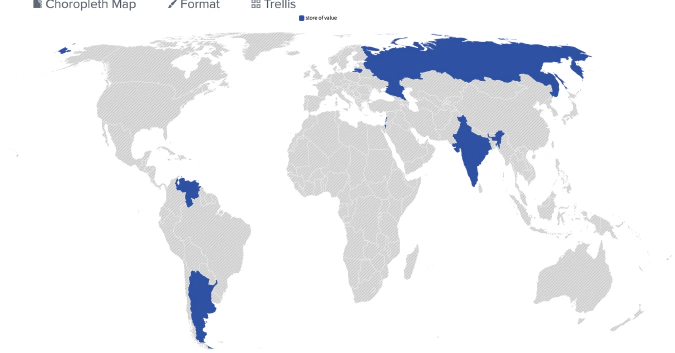

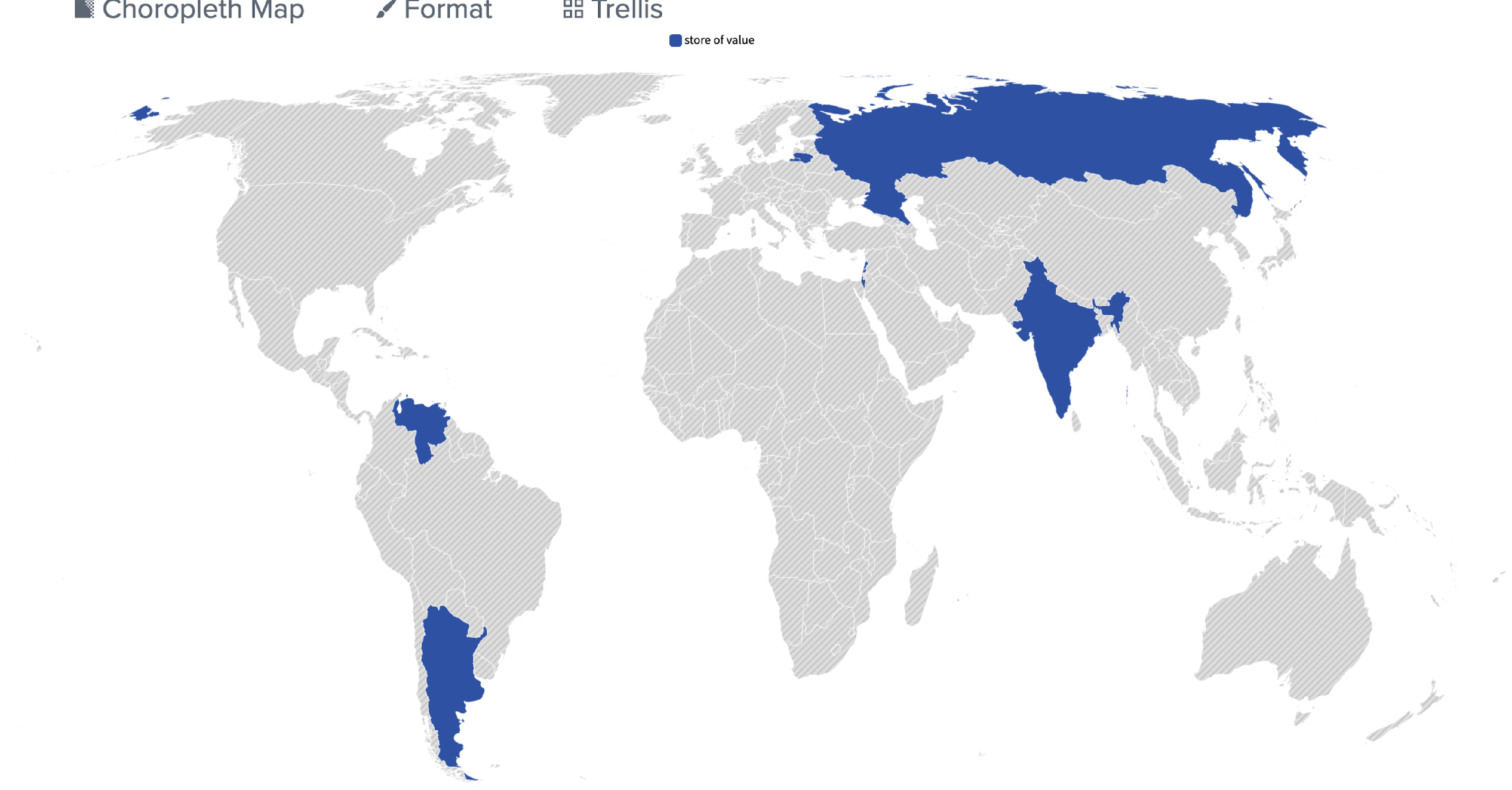

Purpose

Looking at CBDC design choices allowed us to better understand the reasoning of central banks and the unique problems they are trying to solve. CBDC use cases can be grouped in 3 main categories: payment system, store of value, and cross-border settlements. Most projects target multiple groups, but in some cases central banks are explicit about their goal of avoiding unintended consequences of specific CBDC use cases. For example, the European Union is concerned about their CBDC becoming a store of value, as it might lead to bank runs in case of financial instability.

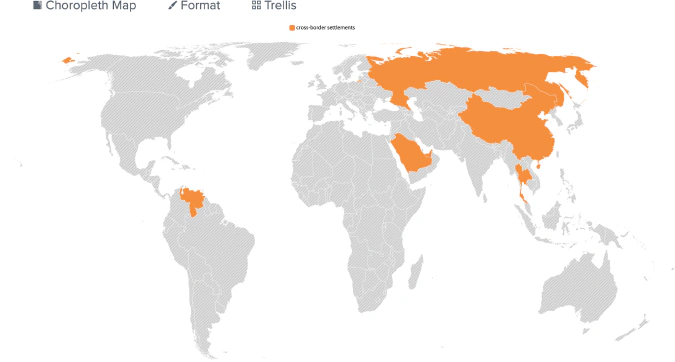

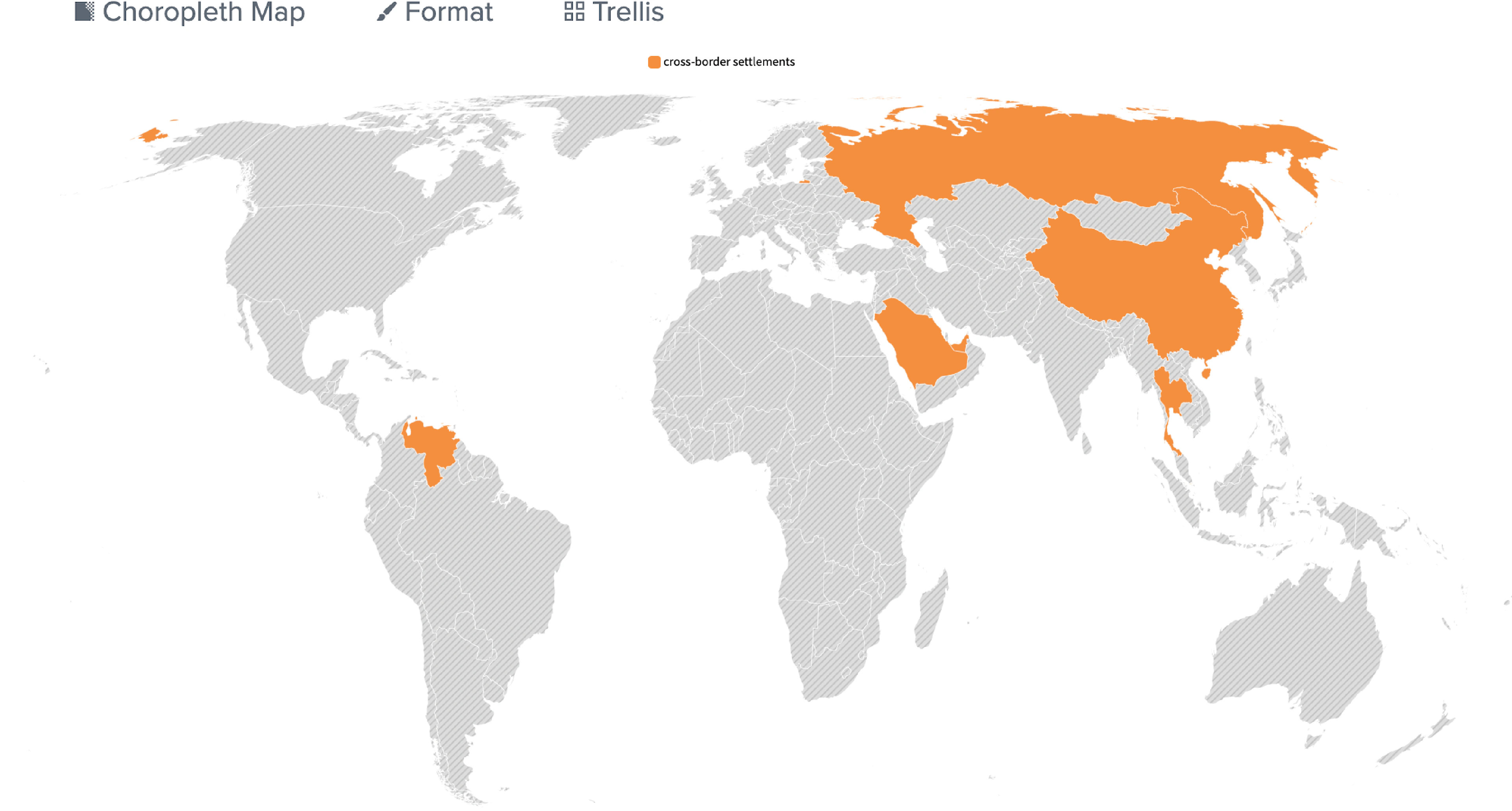

Cross-border settlements is one of the initial go-to use cases. Many governments see problems with their dependence on the US Dollar as a base currency. The ability to efficiently settle trade payments and loans without touching other currencies and payment systems is what is pushing the development of CBDCs in large exporting economies and those under heavy sanctions.

CBDC as a payment system gives issuers better visibility into market activity and extends their reach to the unbanked. This use case attempts to address a growing concern about the transaction information collected by payment service providers, which are predominantly located in the US and Europe.

CBDC as a store of value unlocks the ability to create sophisticated economic policies, easily automating distribution and tax collection. Smart contracts can provide additional dynamics and adaptive incentives to further influence how the money is being used. This use case also creates investment opportunities outside a central bank’s jurisdiction, allowing outside investors to participate in the economy by using the CBDC as a reserve currency. Using CBDCs as a store value usually requires a sound monetary system capable of resisting market manipulation and volatility.

Evidence of Use

At the core of the CBDC Factbook is a number of difficult-to-manipulate adoption metrics that allow us to separate what is being said by CBDC issuers from what is actually being achieved. Examples of such metrics include:

Integrations with existing payment systems or ledgers

Upper-layer products built on top of the CBDC (wallets, payment processing terminals, financial products)

Technological capability

Job openings for relevant software development specialists

Public profiles of residents mentioning relevant technologies

Reputable named entities involved (IT companies, engineers, tech hubs)

Evidence of advanced usage (forensics, surveillance, smart contracts, derivatives)

Publicly available use statistics

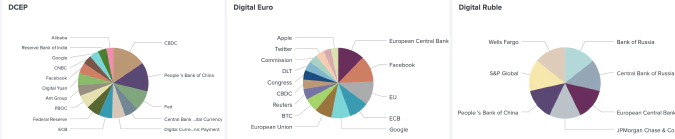

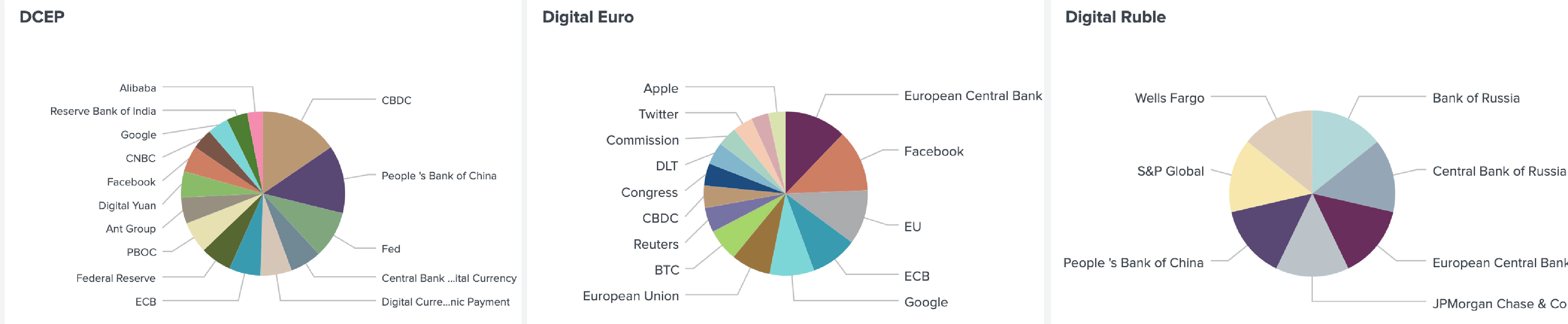

Non-state actors

The Factbook also recognizes non-state actors as potential CBDC issuers. These non-state actors might include IT companies, non-sovereign regions striving for independence, and even terrorist organizations. Some of them have attempted to issue their own money in the past and are sometimes better positioned for their CBDC to be recognized than those of official central banks. As an example, Facebook has a much wider adoption than any existing world currency, which makes its Diem (Libra) project a serious competitor to any CBDC project, regardless of Facebook’s current choice of currency baskets. Tether is already acting as a full-fledged CBDC, both technologically, through the use of an existing smart contract ecosystem, and organizationally, managing fiat money flow and freezing illicit accounts. A region like Catalonia, with their Barcelona tech hub, can easily spin up their own CBDC, especially in case of continuing dissatisfaction with Spanish and EU economic policies.