Summary

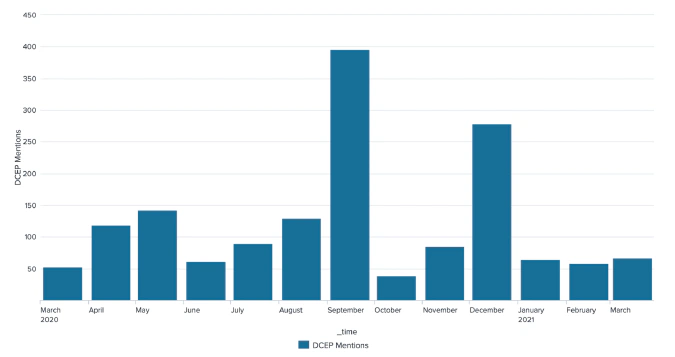

China’s Digital Currency Electronic Payment (DCEP), also known as Digital Yuan, e-CNY, and Digital RMB, is a form of centralized CBDC designed to replace cash in circulation as well as streamline cross-border payments. Far along in its development process, it already features comprehensive regulation and sophisticated pilot projects involving major Chinese banks and internet giants. As of November 2020, these pilot projects already exceeded $300M exchanged in 4 million transactions. The DCEP initiative is fueled by China’s concern over US Dollar dominance, the Belt and Road Initiative, and the upcoming 2022 Winter Olympics in Beijing.

Combining all the technological advances, legislation efforts, and other blockchain initiatives, China is exemplifying a balanced and systemic approach to the development of a CBDC. Although Chinese CBDC project still needs to prove its viability outside of the government sandbox, People’s Bank of China (PBoC) is well on track to have a fully functioning system by the 2022 Winter Olympics in Beijing. It even aims to enable foreign visitors and athletes to use DCEP at the event.

Regulations

Digital Yuan has been given the same legal status as the physical currency. The government decreed that all the merchants who accept digital payments must accept DCEP.

China started the work on its CBDC project in 2014, when Xiaochuan Zhou, then the governor of the People’s Bank of China, established the Digital Currency Research Institute. In 2020, PBoC started pilot tests in a number of provinces.

At the 2020 G20 summit, China’s leader Xi Jinping mentioned the global need “to discuss developing the standards and principles for central bank digital currencies with an open and accommodating attitude, and properly handle all types of risks and challenges while pushing collectively for the development of the international monetary system.”

The October 2020 bill gave the government an exclusive right to issue yuan-pegged stablecoins and criminalized similar activity held by any other non-government institution. If violated, the law imposes fines up to five times the amount of the tokens created and the seizure of the tokens and any profits that their release has produced. The government opened the bill for comments on October 23, 2020.

The bill fits the bigger narrative. According to the documents from the Fifth Plenum Communique, one of the main goals for the upcoming five-year plan is to accelerate the development of the digital economy in general and to advance the research and development of digital currencies in particular.

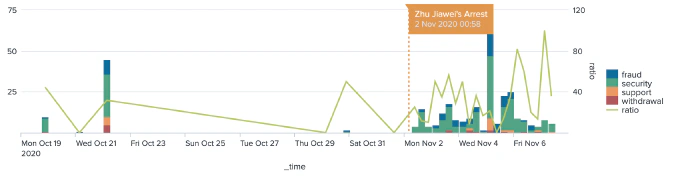

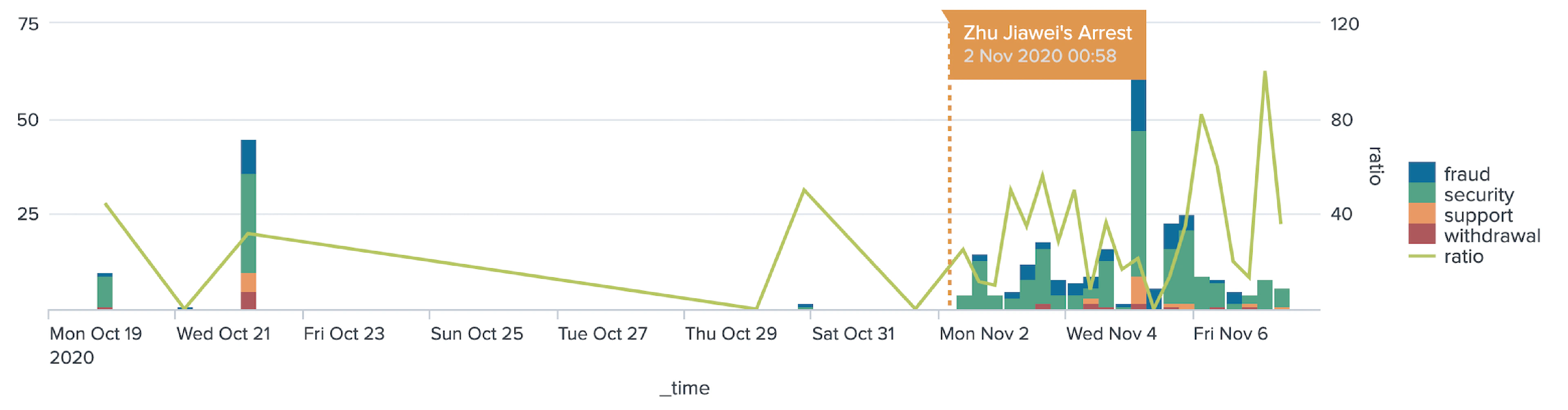

China has also been clearing the playing field from potential competitors to the CBDC ecosystem, prohibiting local cryptocurrency exchanges, banning ICOs, blocking foreign websites related to cryptocurrency and ICOs, driving node validators (miners) out to other countries with new regulatory burdens, and arresting Chinese nationals linked to crypto custody businesses. These actions not only increase volatility of other cryptocurrencies, but also affect the general population’s perception of them by introducing so-called FUD (fear, uncertainty, and doubt) into the market. For example, a spike of fraud- and security-related messages in the crypto community was detected for almost a week after the news of the Chinese crypto-executive arrest spread over the mainstream media.

Issuance

China’s Digital Currency Electronic Payment (DCEP), also known as Digital Yuan, e-CNY, and Digital RMB, is designed to replace cash in circulation. The People’s Bank of China is responsible for the token issuance.

Custody

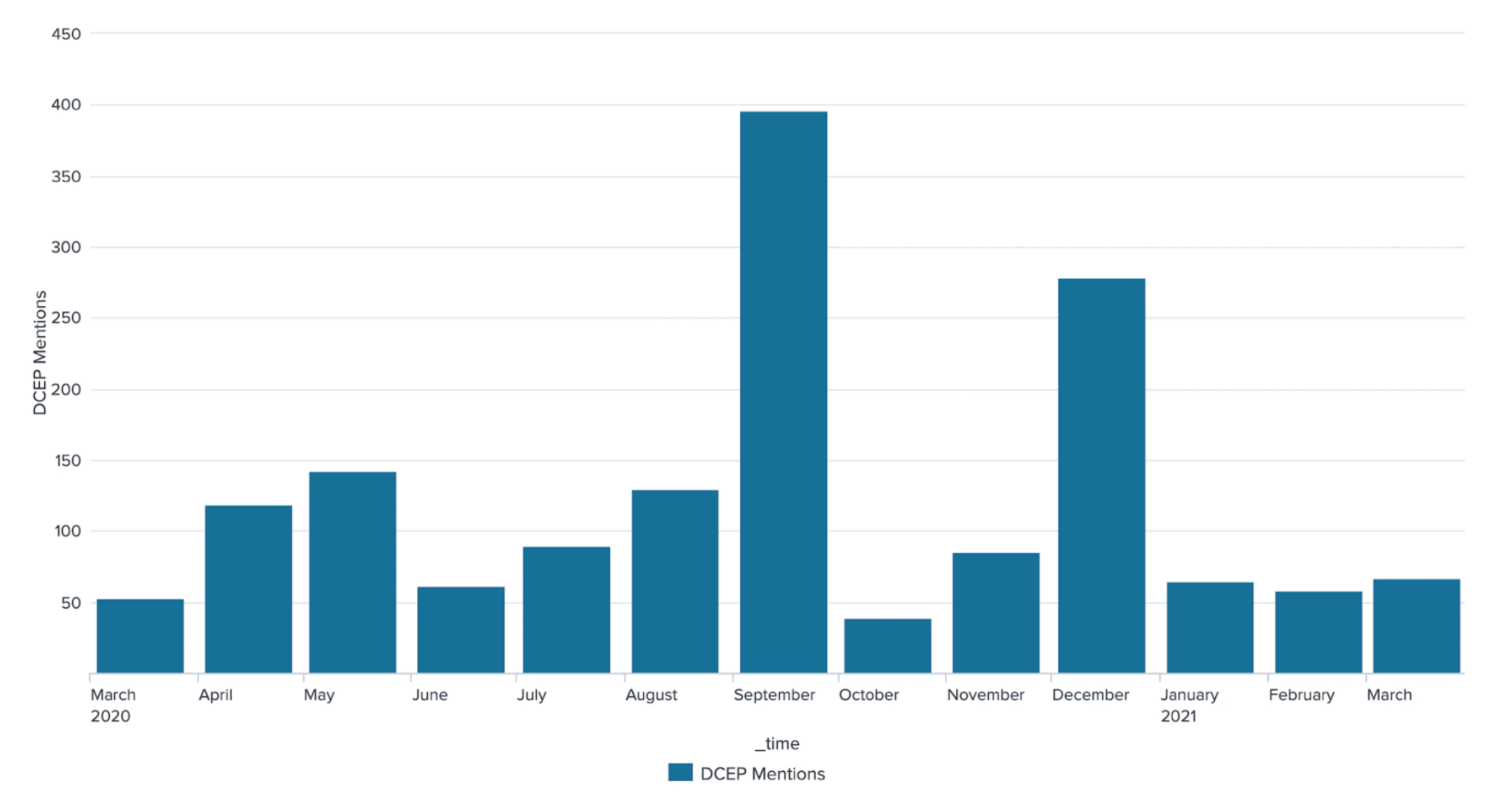

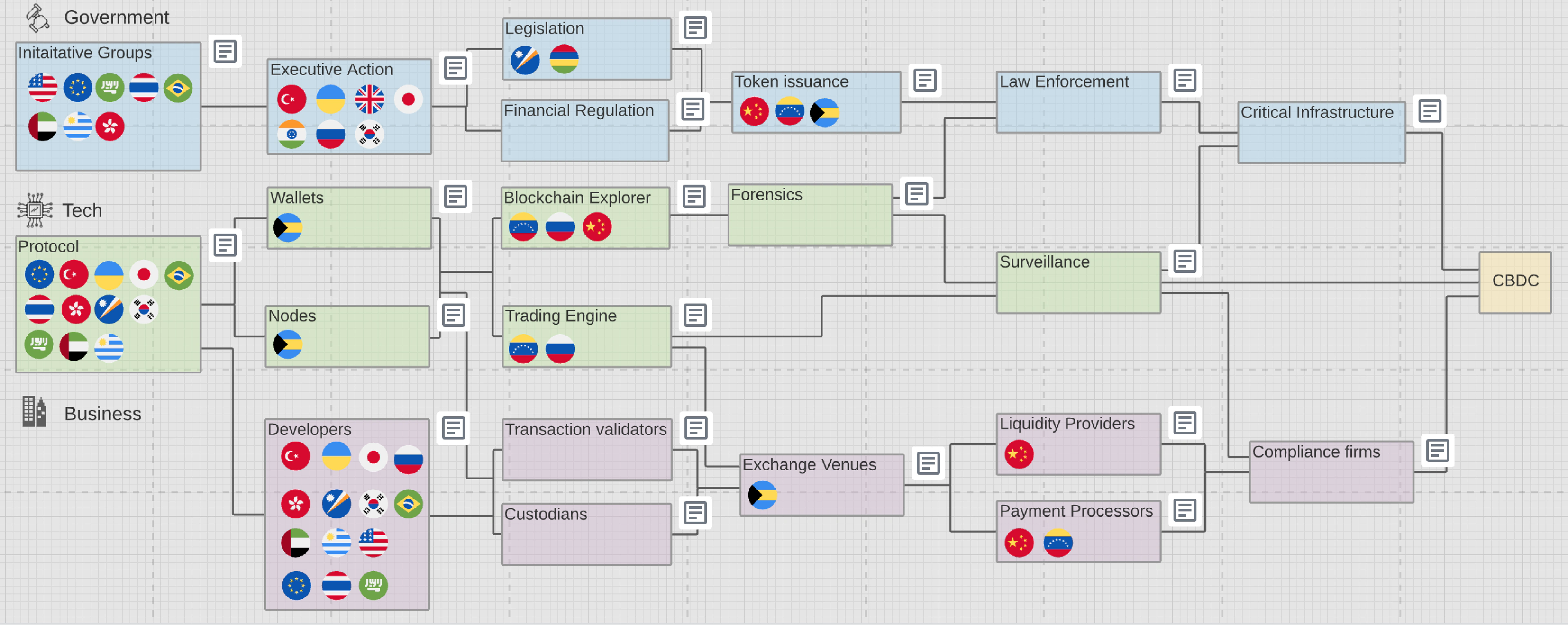

Digital Yuan is issued by the People’s Bank of China and distributed to other banks. As of February 2021, six state-owned banks act as custodians in this system: China Construction Bank, Agricultural Bank of China, Bank of China, Industrial and Commercial Bank of China, Bank of Communications, and Postal Savings Bank of China.

According to the local media report, China Merchants Bank and Hong Kong-based China CITIC Bank joined the system and are in the process of introducing their digital wallets.

Distribution

The DCEP has a two-tier distribution system. The first system is tasked with distributing the currency between the central bank and commercial state-owned banks, as well as large fintech companies. The other system is responsible for interconnecting commercial banks with individuals and businesses. Digital Yuan can be transferred from the bank accounts of the eight commercial banks mentioned above straight into customers’ wallets or special apps developed by the same banks. To distribute the funds to the customers, these commercial banks must deposit the same amount of CBDC with PBoC. Both the central bank and the commercial banks keep databases that track the flow of funds from one user to another.

Digital Yuan will also be distributed to local fintech companies like Tencent and Alibaba to be used in WeChat Pay and AliPay mobile payment systems, respectively. During the initial stage of pilot testing, Digital Yuan was distributed via multiple lottery airdrops directly into users’ digital wallets. In February 2021, Beijing alone accounted for $1.5M worth of Digital Yuan handed out as a part of the Lunar New Year pilot project.

Technology

The Chinese government chose the centralized CBDC architecture, allowing them to have full control over which transactions make it to the ledger and giving them the ability to deactivate wallets at any time. The People’s Bank of China has filed more than 80 patent applications on its CBDC. The pilot test started in 2020 in Shenzhen, Chengdu, Suzhou, and Xiongan provinces. More provinces — Shanghai, Hainan, Changsha, Qingdao, Dalian, and Xi’an — will join the pilot test in 2021.

Going beyond just technical issues of creating Digital Yuan, the government also focuses on building the infrastructure around its CBDC. The three organizations responsible for maintaining DCEP are:

Identification Center (onboarding new users via KYC rules and issuing credentials);

Record Center (recording issuance and transfers for distributing this data to the nodes);

Big Data Analytics Center (KYC and AML risk management).

The early inclusion of Chinese tech giants with experience in digital payment solutions, namely Tencent and Alibaba, provided the required technological expertise for the creation of CBDC wallets and a payment system. As of February 2021, MYbank and WeBank, backed by Ant Group and Tencent, respectively, are also joining the pilot test alongside the eight major Chinese state-owned commercial banks. Their wallets will be added to the People’s Bank of China’s Digital Yuan app, which can be used to pay for goods and services. International companies like Starbucks, McDonald’s, and Subway are also participating in the pilot testing along with local businesses.

Usage

In November 2020, there had already been approximately $300M worth of digital currency spent in about 4 million transactions. At the beginning of 2021, China rolled out the ATMs to convert cash to and from digital tokens and even biometric hardware wallets. The Agricultural Bank of China launched a pilot ATM project to enable citizens of Shenzhen to convert cash to and from Digital Yuan. The bank has also rolled out accompanying hardware wallets, contactless cards, and wearables.

Digital Yuan can be downloaded into users’ wallets from the bank accounts of the eight state-owned banks (China Construction Bank, the Agricultural Bank of China, the Bank of China, the Industrial and Commercial Bank of China, Bank of Communications, Postal Savings Bank of China, China Merchants Bank, and Hong Kong-based China CITIC Bank). Other banks in the country are also working on apps for the People’s Bank’s digital currency initiative.

Money transmission

On January 16, 2020, the Digital Currency Institute (DCI) of the People’s Bank of China set up a joint venture with SWIFT called the Finance Gateway Information Services Limited. Other shareholders included China’s Cross-border Interbank Payment System (CIPS) and the Payment & Clearing Association of China. The joint venture is focusing on information systems aggregation, data processing, and technology consultancy.

In December 2020, the Hong Kong Monetary Authority stated it was working with the PBoC’s Digital Currency Research Institute to explore the feasibility of starting cross-border clearing and payments. In February 2021, central banks of China, Hong Kong, UAE, and Thailand joined the “Multiple Central Bank Digital Currency Bridge” (m-CBDC) project. The project explores the possibilities of CBDC and DLT-enabled cross-border, multi-currency payments.

Appendix

Key people

Xiaochuan Zhou, former governor of the People’s Bank of China

Yao Qian, former head of the PBOC’s Digital Currency Research Initiative and current Director at the China Securities Regulatory Commission (CSRC)

Di Gang, People’s Bank of China (PBOC) governor

Li Hong Gang

Pan Li

Xi Xu Liang

Zhao Xin

Li Lian San

Du Yan

Huang Lie Ming

Jiang Guo Qin

Sun Hao

Chen Hai Bo

Qian You Cai

Zhao Xin Yu

Wang Xu Wei

Peng Feng

Key organizations

Digital Currency Research Institute of the People’s Bank of China

Hong Kong Monetary Authority

Finance Gateway Information Services Limited

Also published on TabbFORUM